Search

Search

Watching This Week: Canadian Canola Production, US Lemon Prices, and US Feed Demand

CLIMATE-COMMODITIES

European Rapeseed Producers in the Driver Seat Again:

Canada’s canola production is likely to be further downgraded as harvest nears. Crops in the country’s top canola-producing province, Saskatchewan, have experienced stress from dry and hot conditions this summer. Worsening conditions in the southwest part of Saskatchewan were identified by a recent NDVI scan, an indicator of vegetative health. However, rapeseed crop conditions in France, Romania, United Kingdom, and Ukraine improved in the past month. European rapeseed oil producers should not only realize greater export potential in 2017, but also capture higher export prices. We recommend agribusiness companies use Gro to closely monitor EU crop conditions and Canadian and Australian rapeseed export prices in the coming week.

FOOD-TRADE

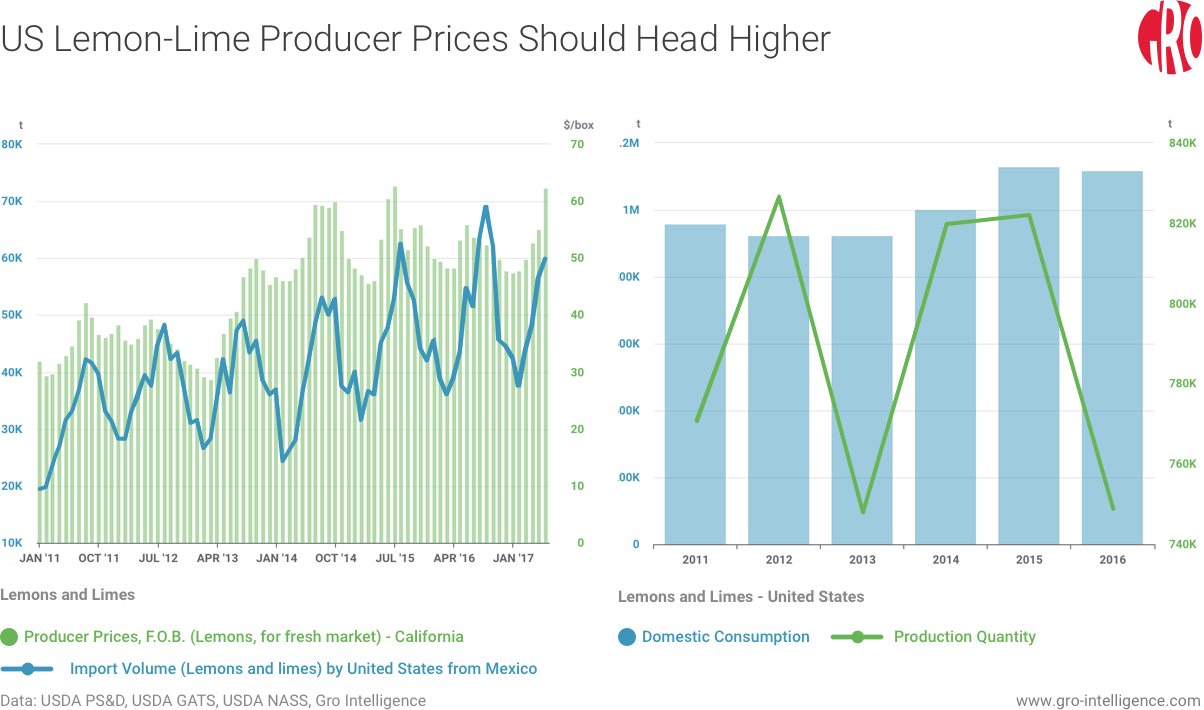

Food Wholesalers Will Face Higher Lemon Prices in August:

Tight US domestic lemon supplies will push wholesale prices higher in August. American lemon and lime demand in 2017 will likely exceed domestic supplies by 350,000 to 400,000 tonnes. Mexico, the US’ top supplier is currently filling the gap, although global competition for available product for export is sharp. Granted, the US lifted its lemon import ban from Argentina in May 2017, but June customs data shows minimal lemon and lime imports to the US from the country. We suggest that retailers keep a close eye on terminal prices along with monthly producer prices in Gro in the coming weeks.

LIVESTOCK-FEED

USDA To Shed More Light on 2017-18 Feed Assumptions:

With the exception of corn, USDA kept feed use assumptions for other major crops unchanged in the August WASDE report. Projected corn use, for feed in 2017/18 was cut by 25 million bushels in the August report. USDA also expects more US beef production in 2017 and 2018 while its outlook pork and chicken production is relatively unchanged. As a result, one could conclude that the 25 million drop in corn use, for feed is based on the assumption of lighter cattle coming to market, lower chicken slaughter rates, or improved feed conversion by livestock in 2017-18. Either way, food and livestock companies will gain more insight into the mechanics of the USDA’s WASDE forecast when the department releases its Feed Outlook report on Monday.

Insight

InsightAvian Flu’s Grip on Egg Prices Is Starting to Crack

Insight

InsightUS Beef Headed for Supply Shock, High Prices Through 2024, Gro Expects

Insight

InsightUS Hogs Supplies to Shrink, Lifting Pork Prices

Insight

Insight